Taxation of Long Term Capital Gains

Taxation of Long Term Capital Gains

The following topics are covered in this blog:

Withdrawal of Section 10(38)

Introduction of Section 112A

What is the concept of Grandfathering?

How does Grandfathering work?

Cost of Acquisition

Examples for better understanding

Tax implication under Grandfathering

Withdrawal of Section 10(38)

In this blog, we will discuss tax implications on Long-Term Capital Gains (LTCG) arising from the sale of below mentioned capital assets:

Listed Equity shares

Equity oriented mutual funds

Units of business trust

Before Budget 2018, Section 10(38) of the Income Tax Act dealt with the taxation of Long-term capital gains on the above-mentioned class of shares.

Long term capital assets

If these shares are held for a period of more than 12 months from the date of purchase, then such shares are said to be Long-term capital assets

Long term capital gain

Gains arising on the sale of such long-term capital assets are called as Long-term capital gains.

As per section 10(38), long-term capital gains on these shares were exempt from Income Tax.

However, Finance Act 2018 has withdrawn the exemption under section 10(38) of the Income Tax Act, 1961 and has introduced a new section 112A in place of section 10(38), which brings LTCG on such shares under the purview of tax with effect from Financial Year 2018-19.

This means that w.e.f 01st April 2018, provisions of Section 10(38) will not be applicable on gains arising on transfer of equity shares, equity-oriented mutual funds, or units of business trust and these will be taxed as per the provisions of section 112A.

Introduction of Section 112A

A new section 112A was introduced in Finance Act 2018, which has become effective from 01st April 2018. It has the motive of taxation of LTCG on the sale of listed equity shares, equity-oriented mutual funds, and units of business trust in a year.

LTCG is:

exempt up to an amount of Rs. 100,000 and

taxable at the rate of 10% on gains exceeding Rs 100,000

Note:

Section 112A will be applicable on the shares on which STT has been paid at the time of purchase and sale.

The benefits of indexation on the cost of acquisition or on the cost of improvements (adjustment to the cost due to inflation) will not be available under this section.

Deduction under section 80C to 80U and rebate under section 87A, if applicable, will not be allowed from the number of capital gains tax under section 112A.

Now, Long term capital loss under section 112A can also be set off from the long-term capital gains under this section.

What is the concept of Grandfathering?

Under section 112A, a Grandfathering clause has been introduced with the intention to provide relief to all those people who have invested in equity shares and equity-oriented mutual funds on or before 31st January 2018.

Grandfathering is a provision in which an old rule continues to apply to some existing situations while the new rule will apply to all future cases.

Those people who are exempt from the new rule are said to have had grandfather rights or have been grandfathered. This clause enables all investors to continue receiving benefits under the old provisions until a limited period of time.

How does Grandfathering Work?

If you have purchased listed equity shares or equity-oriented mutual funds on or before 31st January 2018 and are selling them after 01st April 2018, then long-term capital gains accruing till 31st January 2018 will continue to be governed by the old provisions, i.e. they shall be exempt. This is done by introducing a provision of deemed cost of acquisition.

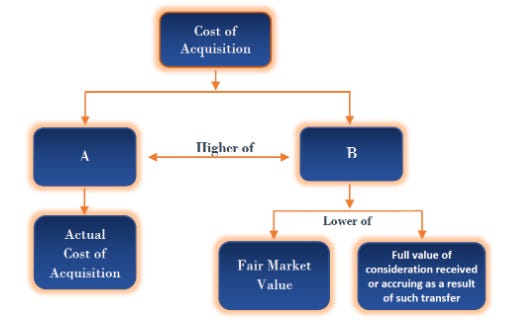

Cost of Acquisition for Grandfathered Cases:

Section 112A has provided a way for computing the Cost of Acquisition for the capital assets that have been acquired before 1st February 2018.

Deemed Cost of Acquisition will be:

Higher of

Actual Cost of Acquisition and

Lower of:

Fair market value – highest price quoted on the recognized stock exchange on 31st Jan 2018

The full value of the consideration received or accruing as a result of such transfer

X bought equity-oriented mutual funds of Rs 1 lakh on 1st February 2010. X sold these funds for Rs 4.25 lakhs on 19 March 2021. Fair market value on 31 January 2018 of these funds was Rs. 3 lakhs. What would be the amount of LTCG liable to tax as per Section 112A?

Since the mutual funds have been held for a period of more than one year i.e. w.e.f. 01st Feb 2018 till 9th March 2019, gains/loss would be long-term capital gain/loss.

Now, to calculate capital gains, first, we need to ascertain the cost of acquisition as per the grandfathering provisions, which is given below

Amount (Rs.)

Higher of:

Actual cost of acquisition 100,000

Lower of Fair Market Value 300,000

Sale value 400,000 300,000

Cost of Acquisition (A) 300,000

Sale value 425,000

Less: Cost of Acquisition (A) 300,000

LTCG 125,000

As per Section 112A, LTCG on sale of equity-oriented mutual funds is exempt up to Rs. 100,000 and taxable @10% on gains exceeding Rs. 100,000. In this case, LTCG up to Rs. 100,000 are exempt and LTCG liable to tax is Rs. 25000.

If the grandfathering clause was not applicable, then the amount of LTCG would have been Rs. 325,000 (Sale price – actual cost of acquisition ie. Rs. 425,000 – Rs. 100,000).

Ex 2: 10th July 2011: Mr. Y purchased equity shares for Rs. 10,00,000

31st Jan 2018: FMV of the shares was Rs. 12,00,000

Sale value is Rs. 15,00,000.

Scenario I: Sold on 1st March 2018

In this case, the purchase was made before 31st Jan 2018, and shares have been sold after 31st Jan 2018 but before 1st April 2018.

Section 112A has been made applicable wef 01st April 2018, therefore, LTCG of Rs.5,00,000 (Rs.15,00,000-Rs.10,00,000) shall be exempt u/s 10(38).

Scenario II: Sold on 2nd April 2018

In this case, shares have been sold after 1st April 2018, thus, section 112A is applicable. Since shares were purchased before 31st Jan 2018, grandfathering would be applicable.

Here, Cost of acquisition would be:

Higher of –

Original COA i.e. Rs. 10,00,000, and

Lower of –

FMV on 31.1.18 i.e. Rs. 12,00,000 #

Sale Price i.e. Rs. 15,00,000

Hence, COA is Rs. 12,00,000

Capital Gain/ (Loss)

Sale Price – Cost of Acquisition

Rs. 15,00,000 – Rs. 12,00,000

Rs. 300,000

The LTCG tax is applicable at a rate of 10% on gains over and above Rs 1 lakh a year. Therefore, LTCG that would be liable to income tax is Rs. 200,000 (Rs. 300,000 – Rs. 100,000)

Tax implications under Grandfathering:

Date of Purchase Date of Sale Tax implication on LTCG

Before 31/01/2018 Before 31/01/2018 Exempt under Section 10(38)

Before 31/01/2018 After 31/01/2018 but Exempt under Section 10(38)

Before 01/04/2018

Before 31/01/2018 On or After 01/04/2018 LTCG Taxable

Grandfathering applicable

After 31/01/2018 On or After 01/04/2018 LTCG Taxable

Grandfathering not applicable